Notes from Pfizer’s 2010 report to investors

Pfizer’s 2010 Financial Report for investors covers a number of topics.

Where does Pfizer sell its drugs? The U.S. represented 42.8 percent of Pfizer’s 2010 sales. Western Europe and Scandinavian countries were 24.6 percent. Australia, New Zealand, Canada, Japan, and South Korea were 14.9 percent. Together, these high income countries were 82.3 percent of Pfizer’s 2010 sales.

Pfizer calls the other Asian countries, plus Africa, Latin America, and Eastern Europe, “emerging markets.” This segment had 17.7 percent of Pfizer sales in 2010, up from 14.9 percent in 2008. In 2010, the “emerging markets” were 72 percent of the sales in Western Europe and Scandinavia, and growing at a faster rate.

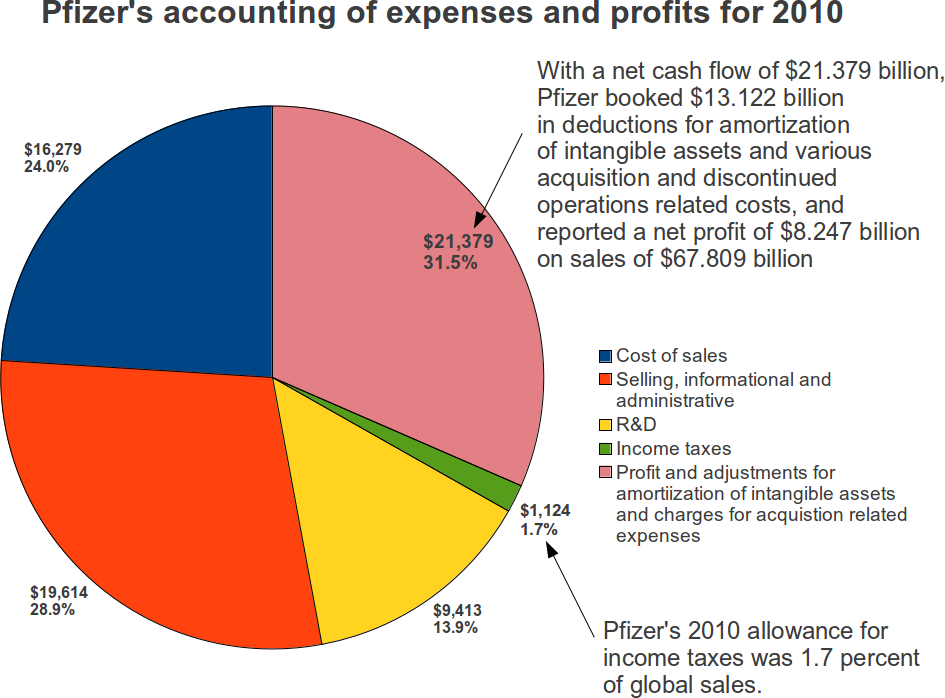

This is how Pfizer reported its major cash flow areas for 2010. Sales of $67.809 billion were offset by $45.306 billion in direct expenses and $1,124 billion in income taxes. The remaining $21.379 was booked either as net income ($8.257) or a variety of amortizations and expenses for intangible assets, and acquisition and discontinued operations expenses ($13.122 billion).

Pfizer’s combined outlays for the cost of sales and R&D were 37.9 percent of sales.

Pfizer gave its shareholders this analysis of the U.S. health care legislation.

Pfizer

Appendix A

2010 Financial ReportPage 3

U.S. Healthcare Legislation

Principal Provisions Affecting Us

In March 2010, the Patient Protection and Affordable Care Act, as amended by the Health Care and Education Reconciliation Act (together, the U.S. Healthcare Legislation), was enacted in the U.S. This legislation has both current and longer-term impacts on us, as discussed below.Certain provisions of the U.S. Healthcare Legislation became effective in 2010 or on January 1, 2011, while other provisions will become effective on various dates over the next several years. The principal provisions affecting us provide for the following:

• an increase, from 15.1% to 23.1%, in the minimum rebate on branded prescription drugs sold to Medicaid beneficiaries (effective January 1, 2010);

• extension of Medicaid prescription drug rebates to drugs dispensed to enrollees in certain Medicaid managed care organizations (effective March 23, 2010);

• expansion of the types of institutions eligible for the “Section 340B discounts” for outpatient drugs provided to hospitals meeting the qualification criteria under Section 340B of the Public Health Service Act of 1944 (effective January 1, 2010);

• discounts on branded prescription drug sales to Medicare Part D participants who are in the Medicare “coverage gap,” also known as the “doughnut hole” (effective January 1, 2011); and

• an annual fee payable to the federal government (which is not deductible for U.S. income tax purposes) based on our prior-calendar year share relative to other companies of branded prescription drug sales to specified government programs (effective January 1, 2011, with the total fee to be paid each year by the pharmaceutical industry increasing annually through 2018).In addition, the U.S. Healthcare Legislation includes provisions that affect the cost of certain of our postretirement benefit plans.

Companies currently are permitted to take a deduction for federal income tax purposes in an amount equal to the subsidy received from the federal government related to their provision of prescription drug coverage to Medicare-eligible retirees. Under the U.S. Healthcare Legislation, effective for tax years beginning after December 31, 2012, companies will no longer be able to take that deduction. While the loss of this deduction will not take effect for a few years, under U.S. generally accepted accounting principles, we were required to account for the impact in the first quarter of 2010, the period when the provision was enacted into law, through a write-off of the deferred tax asset associated with those previously expected future income tax deductions. Other provisions of then U.S. Healthcare Legislation relating to our postretirement benefit plans will affect the measurement of our obligations under those plans, but those impacts are not expected to be significant.

Pfizer also provides this quite general analysis of pricing and access pressures, focusing mostly on Europe and on the threat the U.S. will negotiate prices for Medicare.

Pricing and Access Pressures––Governments, managed care organizations and other payer groups continue to seek increasing discounts on our products through a variety of means such as leveraging their purchasing power, implementing price controls, and demanding price cuts (directly or by rebate actions). In particular, as a result of the economic environment in Europe, the industry has experienced significant pricing pressures in European markets. There were government-mandated price reductions for certain biopharmaceutical products in certain European countries in 2010, and we anticipate continuing pricing pressures in Europe in 2011. Also, health insurers and benefit plans continue to limit access to certain of our medicines by imposing formulary restrictions in favor of the increased use of generics. In prior years, Presidential advisory groups tasked with reducing healthcare spending have recommended and legislative changes have been proposed that would allow the U.S. government to directly negotiate prices with pharmaceutical manufacturers on behalf of Medicare beneficiaries, which we expect would restrict access to and reimbursement for our products. There have also been a number of legislative proposals seeking to allow importation of medicines into the U.S. from countries whose governments control the price of medicines, despite the increased risk of counterfeit products entering the supply chain. If importation of medicines is allowed, an increase in cross-border trade in medicines subject to foreign price controls in other countries could occur and negatively impact our revenues.

On page 7 of the financial report, Pfizer offers this generic comment:

We continue to aggressively defend our patent rights against increasingly aggressive infringement whenever appropriate (see Notes to Consolidated Financial Statements—Note 19. Legal Proceedings and Contingencies), and we will continue to support efforts that strengthen worldwide recognition of patent rights while taking necessary steps to ensure appropriate patient access. In addition, we will continue to employ innovative approaches to prevent counterfeit pharmaceuticals from entering the supply chain and to achieve greater control over the distribution of our products, and we will continue to participate in the generics market for our products, whenever appropriate, once they lose exclusivity.